Main Takeaway: Rising interest rates are pushing prime multifamily capitalization (cap) rates higher in Q3. Despite the upward pressure on cap rates, multifamily assets remain a favored investment type, given the narrowing spread and robust rent growth in select metros.

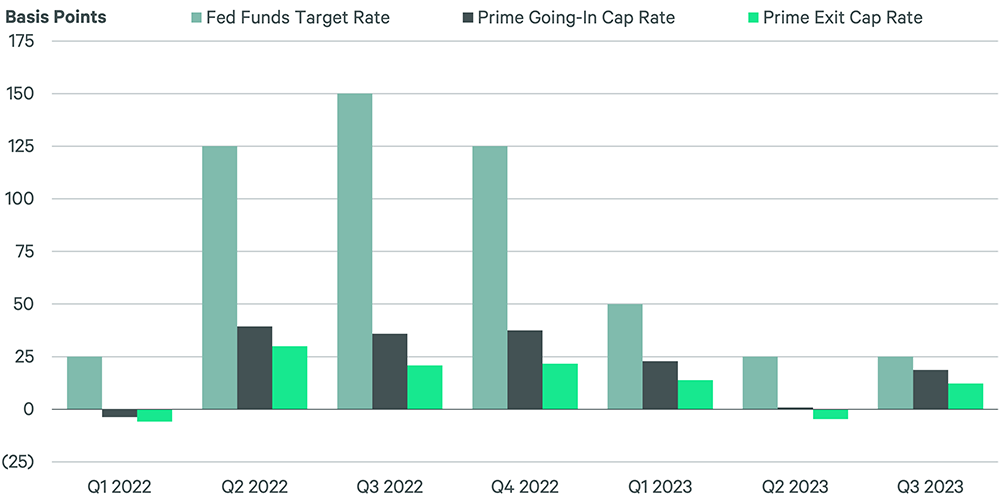

Story: In the wake of the Fed’s 25-basis-point move in July and the 10-year Treasury yield’s seemingly unstable ascent, our prime multifamily assets saw an increase in cap rates in Q3.

While we believe these cap rates might be hitting their high note, don’t be shocked if they shimmy up more into early 2024, especially if rates or bond yields keep dancing upwards. Indeed, according to a new report from CBRE, since Q1 2022, the typical prime multifamily cap rate jumped 155 basis points to 4.92%, outpacing the pre-COVID 2018-2019 average by 70 bps.

While we might see some more growth, especially if the Fed opts for another rate hike in November or long-term rates keep on the upward trajectory, projections for prime multifamily assets seem nearing their zenith.

While the current multifamily cap rate spread is the smallest since 2014, according to Globe St, viewing this in the broader context of the investment market is crucial. A tighter spread doesn’t always indicate diminishing profitability; sometimes, it reflects the inherent strength of the asset class in a volatile environment.

The dance between interest rates and cap rates isn’t a simple mirror image. Cap rates have held their ground, notably in the multifamily and industrial arenas, instead of echoing interest rates. But, according to JPMorgan Chase, price growth coupled with ongoing hikes in interest rates have pushed cap rates to rise in both Q2 and Q3 of 2022.

Drawing from YieldPro, cap rates have shown an overarching trend towards heightening throughout Q3. This phenomenon is largely due to macroeconomic factors and the natural evolution of the real estate cycle. The data shows that we may have also seen peak rent growth.

Despite a slight cooling in cap rates, NorthPeak CRE cites that multifamily assets remain an investor darling. Many attribute this to the sector’s resilience, even in economic downturns, the ever-present demand for housing, and the robustness of rent growth.

Indeed, Gray Capital comments on the robustness of the multifamily sector:

“On one hand, this does make sense a little bit. The steady conditions of the apartment market will likely bring investors into the market, but on the other hand, if there is a critical mass of apartment owners that are compelled to sell because they’re facing steep interest rate increases, we could see a moment, maybe not a whole year, in 2023 where cap rates expand more than 10 bps.”

All that said, Multihousing News provides a promising picture for 2023, suggesting substantial rent growth. This growth and steady occupancy of 95% can offset some challenges of rising cap rates.

While the pulse of cap rates has certainly quickened, the multifamily sector continues to offer a rhythmic dance of opportunities for those keen to tune in and adapt. Investors need to take from the current economic environment that the multifamily beat goes on, as does the allure of multifamily investments.

Expert Take on Multifamily Cap Rates

“The increase in mortgage rates that might normally support the business has become a burden, rising from an average 3.4% on 7-to-10-year fixed rates in October 2021 to 5.5% of June 2020. That’s a 210-basis point shift, but multifamily cap rates only increased 40 basis point to 5.1% in August 2023. Prices peaked in July 2022 and have been sliding since then, with the RCA CPPI for apartments down 14.9% from a year earlier in August.” — Erik Sherman, Globe St