Main Takeaway: Deals are getting repriced at record levels. Despite that, sentiment among owners and investors is robust, but they should still expect higher price variability in the short term as debt costs and inflation stay elevated.

Story: NMHC reported in their Quarterly Survey of Apartment Construction & Development Activity that 76% of multifamily developers reported experiencing deal repricing over the last three months ending Q4 2022.

A sizeable portion of respondents reported using alternative brands or suppliers to mitigate price increases and supply shortages for exterior finishes and roofing (46%) as well as for appliances (30%). For the second-straight quarter, respondents reported utilizing escalation clauses at lower rates than in the previous quarter for all materials.

Paul Bergeron of Globe Street comments on this construction data, noting that deal repricing is actually stabilizing from pandemic levels where supply chains and labor shortages were at record highs. Paul Rahimian, CEO and founder of Parkview Financial, says:

Development has slowed somewhat with increased costs of debt, as well as the pullback by construction lenders to fund new projects…Further supply chain constraints have been severely reduced, allowing for extra material supply in some sectors. We have recently noticed that construction costs are either stagnant or increasing at a very low rate compared to the past seven years. As such it is possible that we will find a reduction of construction costs on the horizon, however, it is too early to tell.

In addition to this, multifamily loan origination in Q4 of 2022 saw a massive decrease of over half year-over-year. Typically, Q4’s see the highest lending volumes; this year, they were down 54% YoY and dropped 23% QoQ.

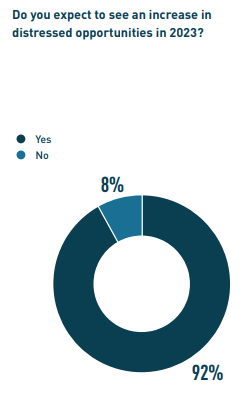

A new survey from Berkadia found that almost all (92%) commercial real estate professionals expect more distressed deals to come online in 2023. This reflects the ongoing sentiment of increased cap rates and deal repricing.

Despite these expectations, Wealth Management comments on the above report noting:

Fifty-four percent believe that rising interest rates and inflation will have an “extremely” pronounced impact on investment sales activity in 2023, and 45% expect a “moderate” impact on sales deals. Yet, at the same time, 59% of Berkadia respondents said that renter demand for apartments will continue to outstrip available supply this year, while 30% expect supply to outstrip demand and 11% are unsure of how the equation will play out.

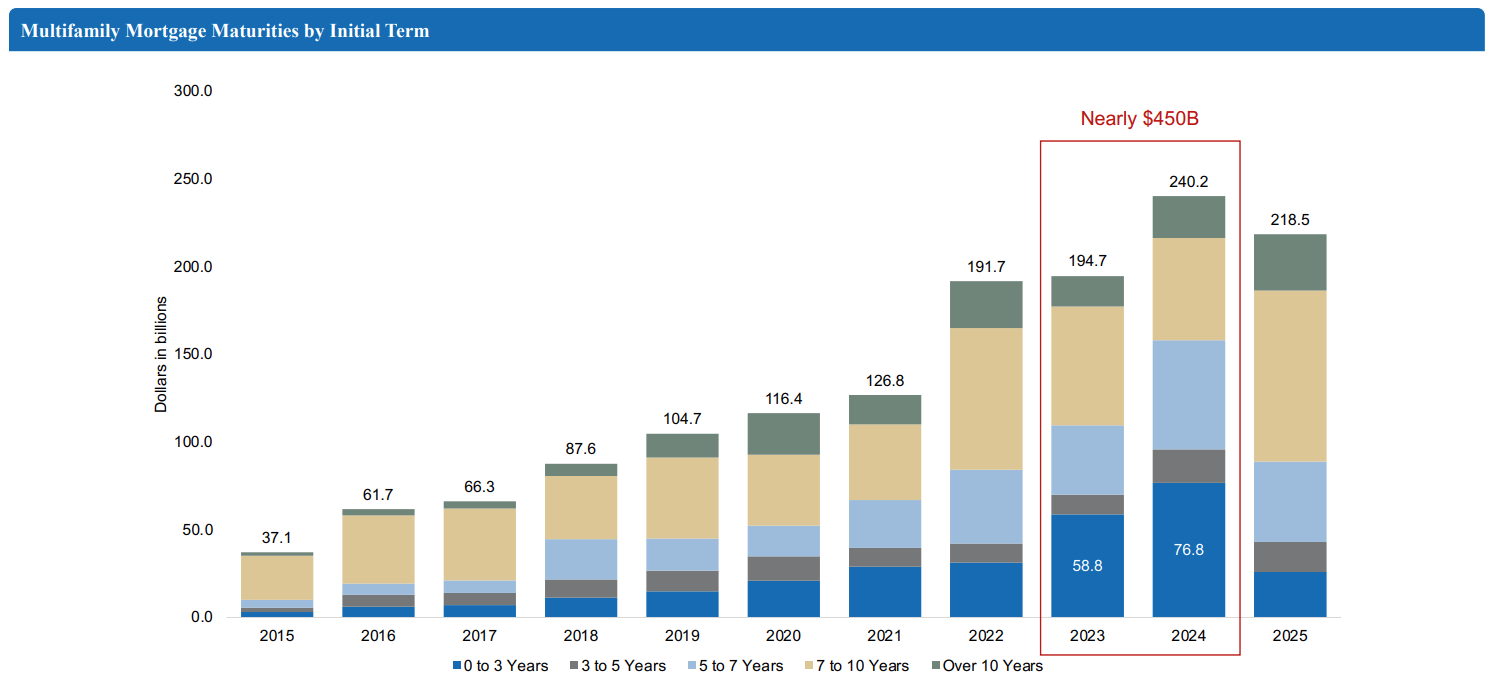

Deal repricing will be further exacerbated by the amount of multifamily debt maturing in 2023 and 2024 amidst higher interest rates, putting downward pressure on prices. According to data, a record $450B is maturing this year and next, highlighting the risk of rising rates and asset valuation.

That said, the same study found that “investor appetite from global sources continues to be deployed into multifamily, as a percentage of total US commercial real estate totaled 40.3% in 2022, up 990 basis points from the 2015-2019 average of 30.4%.

Nevertheless, the era of free money is over, and in previous years owners and investors weren’t pricing in the higher risk of debt costs. Now, they are being forced to, and it is causing a recalibration of asset prices across the board. The multifamily market may move from overperformance over the past few years to more equilibrium between supply, demand, and pricing.

This means buyers who can pencil and underwrite deals in the current market have an advantage in purchase negotiations.

Expert Take on Multifamily Deal Repricing

“Rising interest rates, inflation and worries of a recession have caused a reset on prices, prompting sellers to accept a less satisfying price or pull properties from the market in hopes of a better offer later. The result has been a drop in deals this spring and summer, with no clear timeline for when the market will recover.” — Ryan Ori, Costar