Main Takeaway: Distress in all commercial asset classes, including multifamily, is rising. Keep a close eye on your debt costs and focus on optimizing NOIs and expenses, as high debt costs and record completions will put downward pressure on asset values into 2024.

Story: Like the entire commercial real estate industry, multifamily owners and investors are worried. Rising debt costs and increasing supply are fueling worries about asset distress. As sophisticated investors, we understand the need to stay informed about the data and trends, both good and bad, in the multifamily market. With that in mind, let’s delve into the challenges for our asset class.

Rising Debt Costs

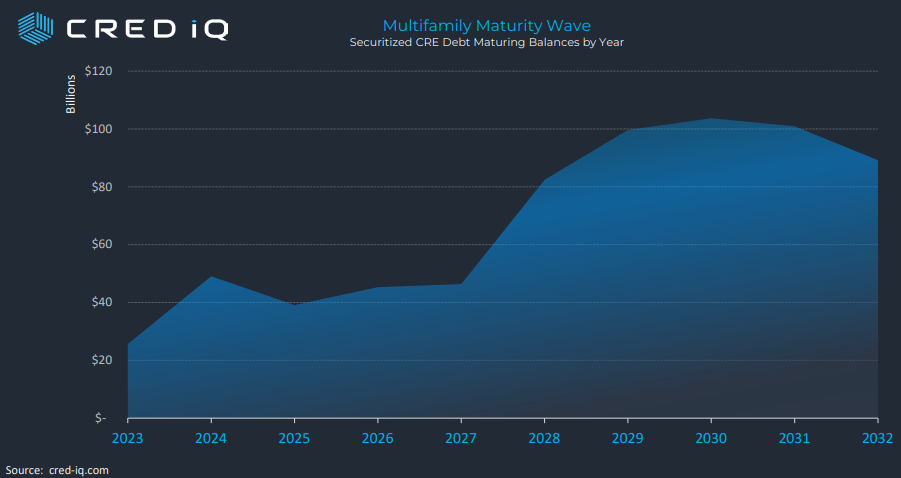

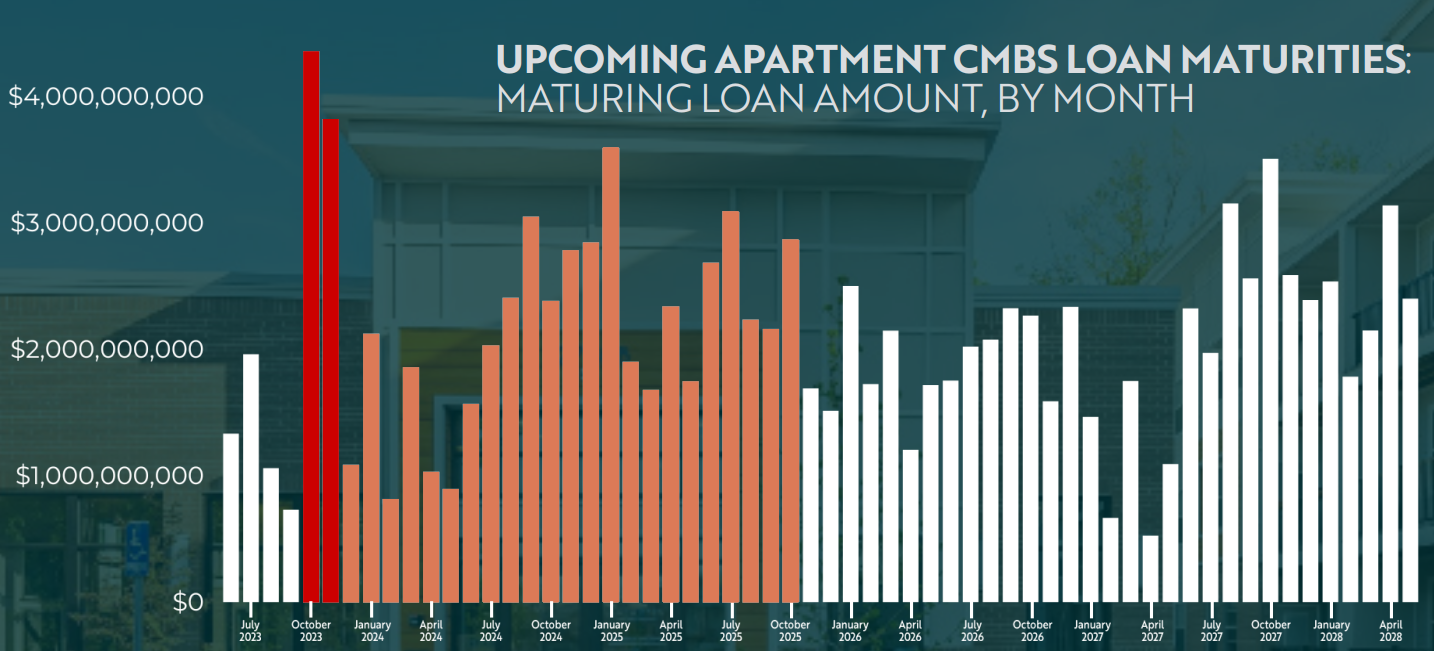

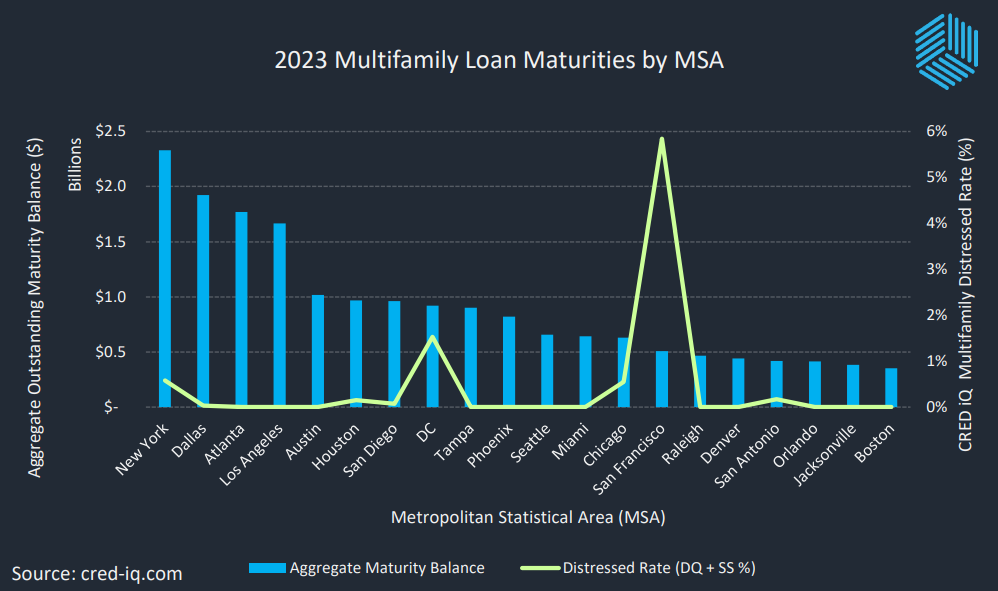

The multifamily sector has recently faced increased pressure due to rising debt costs. According to a report by CRED iQ, a comprehensive real estate finance data source, more than 2,300 multifamily loans with a 2023 maturity date totaling approximately $25 billion are set to mature. Many of these loans were obtained with sub 3% loans, now needing refinancing at 6%+.

This impending “maturity wall” has drawn significant attention from market participants, posing a potential challenge for property owners and investors. In October and November alone, we will see a full $8B of multifamily debt come to maturity.

Undoubtedly, we will see an increase in distressed assets across the commercial space, including multifamily.

Increasing Multifamily Supply

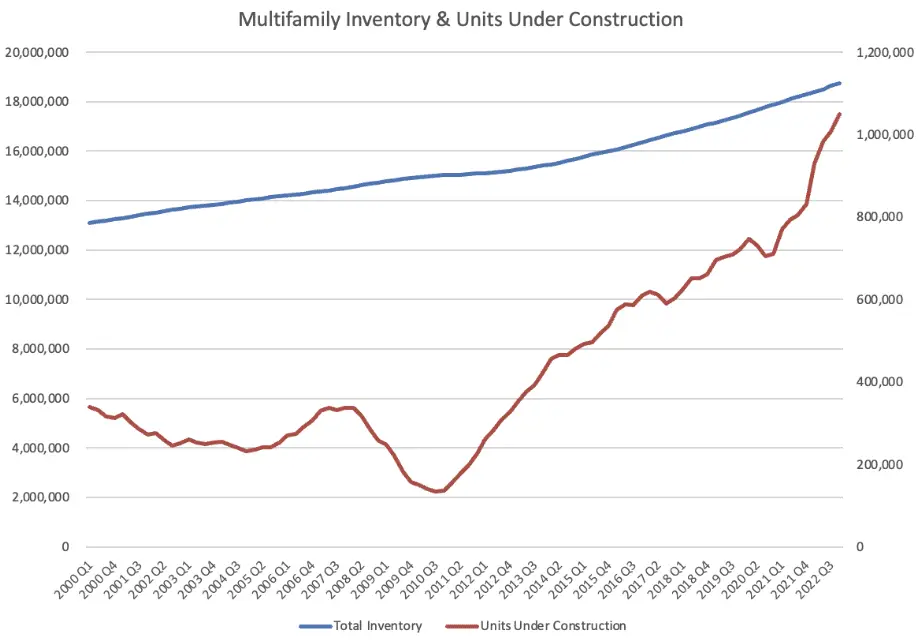

According to the National Apartment Association (NAA), “a record number of new construction apartments will reach completion, with 2023 deliveries forecast to reach highs not seen since the mid-1980s. A whopping 500,000 new units are expected to hit the market this year, with elevated deliveries continuing into next year.”

Since 2010, we’ve seen a gradual increase in the supply of new multifamily developments, and for the first time, we’ve surpassed over 1 million units under construction.

Increases in supply tend to put downward pressure on rents, NOIs, and ultimately valuations. Now this isn’t a perfect relationship, and an increase in rates also means homeownership will be unattainable for many, keeping them in the rental market and increasing demand.

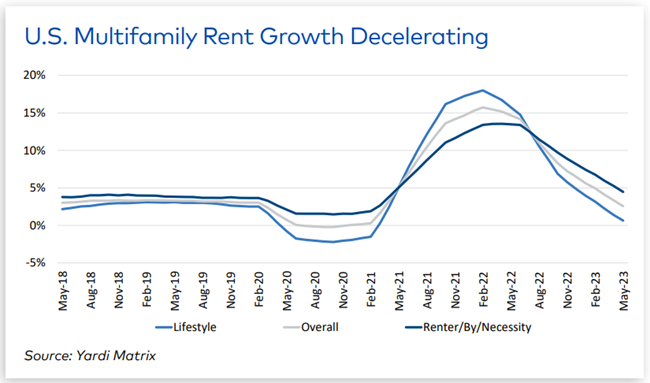

Rent Growth Slowing

Most rent tracking outlets, including Zumper, Apartment List, and Redfin, all report a deceleration of rent growth across the board. Although rent growth is still in positive territory, it has been decelerating over the past 12 months.

Source: Yardi Matrix

Where and When Will Distress Hit?

Trepp reports on the forthcoming distress in our market, noting that San Francisco has the highest multifamily delinquency rate of all metros at 2.69%. New York, Pittsburgh, Philadelphia, and Houston follow suit at 1.01%, 0.82%, 0.70%, and 0.62%, respectively.

“Trepp also tracks the percentage of loans where debt service coverage is less than 1 (DSCR < 1). For multifamily properties, San Francisco leads again, with a rate of 12.98%. Interestingly, three big Texas cities all rank in the top five, with Dallas, Houston, and San Antonio posting rates of 9.15%, 9.03%, and 7.59%, respectively.”

According to CRED iQ, the markets with the most exposure to multifamily loan maturities are New York, Dallas, and Atlanta, respectively, with San Francisco currently witnessing the highest number of distressed loans.

While distress is expected to vary across markets, knowing potential risk factors can help investors make informed decisions and navigate these challenging times.

But, Demand Remains Steady

Despite the challenges, demand for multifamily properties remains steady. The rental market continues to show resilience, with a consistent need for housing nationwide. According to Globe St, in Q2 2023, net demand for apartments hit a five-quarter high, with completions of roughly 1 million assets expected throughout the remainder of 2023 and into 2024.

“Net new demand is occurring most in the Sun Belt or Mountain region but also in some Mid-Atlantic areas, with Houston ranking first, followed by Phoenix, Dallas/Fort Worth, Charlotte, Nashville, Austin, Atlanta, Washington, D.C., and Orlando in the top 10 spots. The next five included Denver, Northern New Jersey, Raleigh/Durham, Jacksonville and Huntsville. Along much of the West Coast, net demand was more limited.”

But expect delays. According to a new NHMC survey, 17% of developers reported that construction labor would be less available than three months ago, up from 10% in March. Further, 90% of respondents reported experiencing construction delays, up from 79% in March and 84% in December.

It is important to note that while the sector may face headwinds, it also presents opportunities for those who can adapt and capitalize on changing dynamics.

The rising debt costs and increasing supply pose several challenges for multifamily owners and investors. If not managed effectively, the distress in the market could result in decreased cash flow, lower property values, and potential defaults for some owners. As a result, it is crucial for investors to stay proactive and develop strategies to mitigate these risks.

Expert Take on Multifamily Distress

“The current economic landscape has made it difficult for multifamily buyers and sellers to transact. While the next 6-12 months are still uncertain, I can imagine a scenario where we witness some real distress all at once, which will create a lot of fear. That may create a window where some incredible assets can be acquired at a significant discount from previous market pricing. Any distress will be short, with interest rates gradually lowering and the base case for multifamily being as strong as ever.“ — Spencer Gray CEO, President, and Co-Founder, Gray Capital